![]()

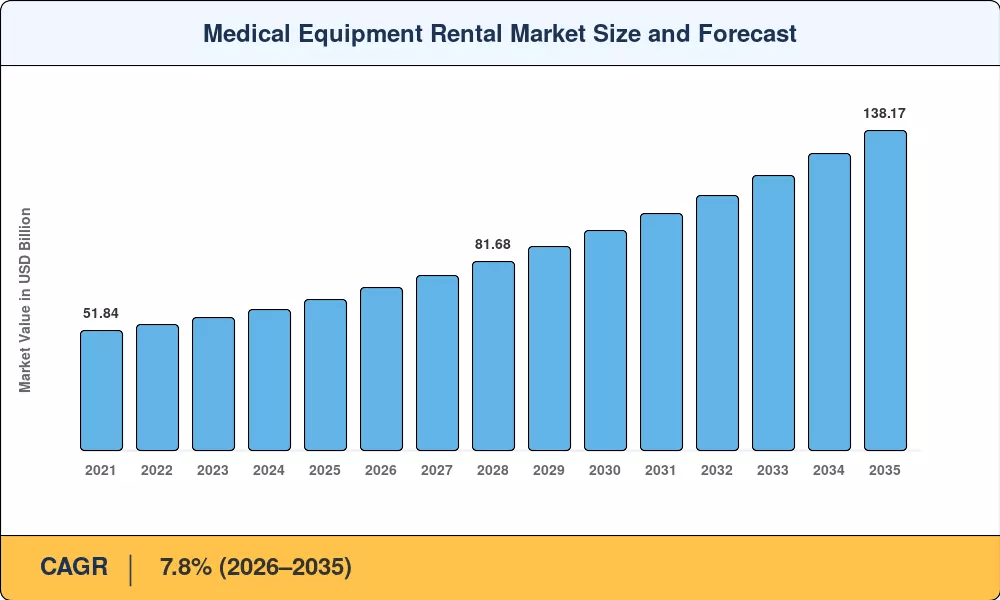

Medical Equipment Rental Market to Surge from USD 70.29 Billion in 2026 to USD 138.17 Billion by 2035—Powered by Hospital-at-Home Reimbursement Expansion

NY, CA, UNITED STATES, June 23, 2026 /EINPresswire.com/ — As per Market Research Future, the global Medical Equipment Rental Market size to reach USD 138.17 Billion by 2035 from USD 70.29 Billion in 2026, at a CAGR of 7.8% during the forecast period 2026–2035. The market base was estimated at USD 65.20 Billion in 2025.

The 7.8% CAGR—anchored by operational flexibility rather than discretionary healthcare spending—is driven by three converging forces: CMS’s Hospital-at-Home waiver program extending acute-care reimbursement to rented bedside devices in over 300 health systems, AI-enabled fleet analytics adoption reducing idle-asset time by 22–28% and compressing technology refresh cycles from seven years to roughly three, and value-based care mandates that have converted capital-intensive equipment procurement from balance-sheet liabilities into per-episode operational expenditures tied to patient outcomes.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/24507

Key Market Trends & Growth Drivers

Hospital-at-Home Reimbursement Expansion

CMS extended its Acute Hospital Care at Home waiver until September 2030, covering more than 300 health systems and 135 qualifying conditions across the United States. This waiver explicitly reimburses the rental of bedside monitors, infusion pumps, and oxygen concentrators delivered to a patient’s residence, converting what was historically a capital-equipment purchase decision into a per-episode rental transaction.

The American Hospital Association estimates the program diverted USD 4.1 billion in inpatient spend toward home-based care in 2024 alone. European parallels—notably France’s Hospitalisation à Domicile scaling to 2.3 million patient-days annually—create a similar rental demand corridor. This driver carries immediate impact because the reimbursement policy directly shifts procurement behavior without requiring new technology adoption.

AI-Enabled Fleet Analytics Adoption

Legacy outright-purchase models—where hospitals locked USD 1.5–8 Million per MRI or CT unit into 10-year depreciation schedules—are giving way to subscription-style rental platforms that embed predictive-maintenance telemetry, IoT utilization dashboards, and automated compliance tracking. AI-driven utilization dashboards help rental operators reduce idle-asset time by 22–28% and minimize maintenance expenses by 15%, according to a 2024 KLAS Research study.

Vendors like Agiliti and Philips now offer platforms that incorporate into a single SaaS layer real-time RFID tracking, predictive-failure alerts, and automated regulatory-compliance checks. Hospitals using these managed-rental systems had equipment uptime above 96% compared with 82–85% for traditional in-house biomedical-engineering models.

Value-Based Care and Bundled-Payment Models

CMS’s Oncology Care Model and its successor, the Enhancing Oncology Model, tie provider reimbursement to outcome metrics that favor operational expenditure over capital commitment. Bundled-payment frameworks for elective surgery explicitly reward facilities that minimize per-procedure equipment costs—a metric that rental models optimize through predictable monthly fees and technology refresh guarantees. The move from capital-intensive purchase to operational rental expenditure decreases balance-sheet leverage, freeing credit capacity for clinical workforce expansion.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/24507

Market Segment Insights

BY DEVICE CATEGORY

Durable Medical Equipment: Dominant segment with ~32.4% revenue share in 2024. Reflecting entrenched Medicare/Medicaid coverage and aging demographics. Wheelchairs, hospital beds, oxygen concentrators, and mobility scooters anchor institutional formularies globally due to well-codified reimbursement and decades of clinical evidence supporting rental over purchase for chronic-care patients. Hospital procurement teams treat durable equipment as a default first-line rental category, and CMS competitive-bidding rates have enabled broad adoption even in cost-sensitive markets.

Surgical and Procedural Equipment: Fastest-growing device category at 6.9% CAGR (2026–2035). Driven by ambulatory surgery center proliferation and robotic-surgery rental adoption. Renting a robotic surgical system at USD 80,000–120,000 per month rather than purchasing at USD 1.8–2.5 Million allows mid-sized ASCs to offer robotic-assisted procedures without the capital commitment. Pipeline expansion in minimally invasive platforms targeting orthopedic and cardiovascular procedures could double the segment’s addressable population by 2030.

BY END USER

Hospitals and Acute-Care Centers: Dominant end user with ~26.2% revenue share in 2024. Comprehensive oncology service lines and seasonal surge management dominate volume. Hospitals remain the primary delivery site for rental equipment due to ICU capacity flexibility—a 500-bed hospital can scale ventilator inventory from 40 to 120 units within 48 hours through rental contracts, a capability institutionalized in emergency-preparedness plans since the COVID-19 pandemic.

Home-care Patients: Fastest-growing end-user segment at 8.4% CAGR (2026–2035). Reflecting post-pandemic reimbursement expansions and patient preference for home-based recovery. CMS Hospital-at-Home waivers and parallel European home-care reimbursement programs create a guaranteed rental revenue stream for qualifying devices. This convenience-driven adoption is expected to open up incremental revenue for the Medical Equipment Rental Market in settings lacking permanent capital infrastructure.

BY SERVICE TYPE

Long-Term Rentals: Dominant service type with ~34.2% revenue share in 2024. Skilled-nursing facilities and chronic-care patients favor predictable monthly OpEx. Contracts typically run 12–36 months and include bundled maintenance, creating stable recurring revenue for operators.

Short-Term Rentals: Fastest-growing service type at 8.9% CAGR (2026–2035). Disaster-preparedness stockpiling contracts and elective-surgery rental bundles drive demand. Hospitals and ASCs increasingly rent specialized equipment for specific surgical campaigns or clinical trials, returning devices once the engagement concludes. This flexibility-driven adoption is expected to open up incremental revenue for the Medical Equipment Rental Market in the absence of permanent capital budgets.

Read Detailed Insights:

https://www.marketresearchfuture.com/reports/medical-equipment-rental-market-24507

Regional Outlook

North America — Dominant Market (~33.5% Share, 2024)

The United States generates approximately 78.2% of North American Medical Equipment Rental Market revenue, driven by CMS’s competitive-bidding program for durable medical equipment, the Hospital-at-Home waiver extending acute-care reimbursement to over 300 health systems, and broad GPO rental frameworks—a single policy ecosystem that converted a capital-purchase-dominated market into one with a structural operational-expenditure tail.

CMS reimbursement for home-care equipment under Medicare Part B has driven adoption across community oncology networks, while academic medical centers increasingly deploy managed-equipment-service contracts to optimize biomedical engineering capacity. The US dominates through a combination of high per-patient spending, robust payer coverage, and rapid AI-fleet-analytics adoption.

Europe — Second Largest (31.4% Share, 2024)

Europe’s Medical Equipment Rental Market reflects deeply entrenched reimbursement pathways. Germany leads regionally with statutory sickness-fund rental reimbursement for home-care equipment, contributing 6.8% CAGR (2026–2035), while the United Kingdom holds 22.4% of regional share through NHS Long Term Plan targets for a 40% increase in managed-equipment-service contracts by 2028.

France contributes ~18.7% of regional share through Hospitalisation à Domicile processing 2.3 million patient-days annually. Italy is growing at 5.9% CAGR on SSN regional rental procurement tenders. Spain contributes USD 2.18 Billion on public-hospital PPP rental models. The Nordic countries hold ~7.4% of regional share on the cross-border Nordic Health Equipment Pool. Russia contributes USD 1.42 Billion on federal equipment-modernization programs.

Asia-Pacific — Fastest-Growing Region (7.1% CAGR, 2026–2035)

Asia-Pacific is the engine of the Medical Equipment Rental Market. China holds the largest regional share with ~32.6% of regional revenue, driven by the 14th Five-Year Plan channeling CNY 180 Billion into county-hospital upgrades with explicit lease-eligibility provisions—instantly extending equipment rental coverage to over 2,800 county hospitals.

India is growing at 8.2% CAGR on the back of PMSSY Phase V rental-first mandates for diagnostic-imaging suites across 22 new tertiary hospitals. Japan contributes 21.8% of regional share through NHI pricing for long-term care insurance rentals covering 6.8 million beneficiaries. South Korea is growing at 6.5% CAGR on National Health Insurance rental coverage expansion.

Middle East & Africa — Emerging Opportunity (USD 3.98 Billion, 2025)

The Middle East & Africa is bifurcated between well-funded Gulf states and resource-constrained Sub-Saharan nations. Saudi Arabia leads the region with Vision 2030 healthcare privatization, contributing ~30.7% of regional share—NEOM health cluster and the UAE’s Cleveland Clinic and Mayo Clinic affiliations have created pockets of excellence for managed-equipment-service contracts.

The UAE is growing at 7.4% CAGR on DHA managed-equipment-service contracts, including a five-year agreement worth USD 320 million covering imaging, surgical, and patient-monitoring devices across 14 public facilities. South Africa contributes 22.1% of regional share on National Health Insurance rental provisions.

South America — Growing Presence (USD 4.04 Billion, 2025)

Brazil anchors South America’s Medical Equipment Rental Market at ~58.4% of regional revenue, with the Unified Health System (SUS) federal procurement tenders increasingly structured as operating leases rather than outright purchases, providing a stable demand floor that smooths regional forecasts.

The Inter-American Development Bank’s USD 800 Million regional health-infrastructure facility requires that at least 25% of equipment procurement budgets flow through leasing or rental channels. Argentina is growing at 5.3% CAGR on provincial hospital PPP leasing.

Competitive Landscape and Recent Developments

The Medical Equipment Rental Market exhibits low concentration, with the top five operators collectively accounting for an estimated 22–28% of global revenue. The Herfindahl-Hirschman Index sits below 600, indicating a fragmented landscape where regional specialists, device-manufacturer rental arms, and independent platform operators compete alongside global players. Consolidation is accelerating, however, as scale advantages in fleet logistics, data analytics, and cybersecurity compliance favor larger platforms.

The competitive landscape is stratified between pure-play rental platforms serving global healthcare markets, OEM-integrated rental arms leveraging device ecosystems, and home-care specialists consolidating the durable medical equipment segment.

KEY COMPANIES AND RECENT MILESTONES

Agiliti (May 2024): Finalized its definitive corporate take-private transaction by private equity firm Thomas H. Lee Partners for an enterprise value of approximately USD 2.5 billion, shifting its operations toward inner-fleet efficiency and comprehensive on-site clinical asset management. Largest U.S.-focused pure-play rental platform, commanding ~5–8% of global Medical Equipment Rental Market revenue.

Koninklijke Philips (2024–2025): Imaging-as-a-service, patient monitoring rentals, and managed technology agreements reinforce the OEM-integrated rental leveraging device ecosystem positioning, holding ~4–6% of global revenue. The company benefits from the structural digital-fleet tail created by expanded AI-analytics platform investment.

GE HealthCare (2024–2025): Imaging equipment leasing and fleet utilization analytics reinforce the OEM rental arm with global service infrastructure positioning, holding ~3–6% of global revenue.

Siemens Healthineers (June 2024): Introduced value-partnership rental contracts for its NAEOTOM Alpha photon-counting CT scanner, enabling mid-sized hospitals to access the platform without capital expenditure. Premium imaging and lab equipment rental positioning, holding ~3–5% of global revenue.

Future Outlook: 2026–2035

By 2030, AI-orchestrated fleet management will become the operating system of medical equipment logistics. The convergence of predictive analytics and autonomous supply-demand matching will reshape the Medical Equipment Rental Market through the late 2020s. By 2030, an estimated 60% of large rental operators will deploy fully autonomous fleet-optimization engines that match equipment supply to demand in real time using hospital census data, elective-surgery schedules, and weather-driven respiratory-admission forecasts.

McKinsey projects that AI-orchestrated logistics can reduce fleet size requirements by 15–20% while improving utilization rates above 90%. The DOE’s supply-chain investments and connected-device telemetry ensure that predictive maintenance scales alongside clinical demand. Machine-learning models that integrate utilization, failure-mode, and patient-acuity data can recommend optimal equipment deployment for individual facilities. Start-ups have raised over USD 800 million in venture funding for healthcare fleet-analytics tools since 2023.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/durable-medical-equipment-market-2676

https://www.marketresearchfuture.com/reports/home-medical-equipment-market-8486

https://www.marketresearchfuture.com/reports/medical-devices-market-2869

https://www.marketresearchfuture.com/reports/patient-monitoring-devices-market-2484

https://www.marketresearchfuture.com/reports/diagnostics-devices-market-68212

https://www.marketresearchfuture.com/reports/healthcare-it-market-5950

https://www.marketresearchfuture.com/reports/medical-supplies-market-2433

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery