![]()

Sepsis Diagnostics Market to Surge from USD 0.91B in 2026 to USD 1.69B by 2035-By Rising Global Sepsis Incidence, Molecular Diagnostics Technology Shift

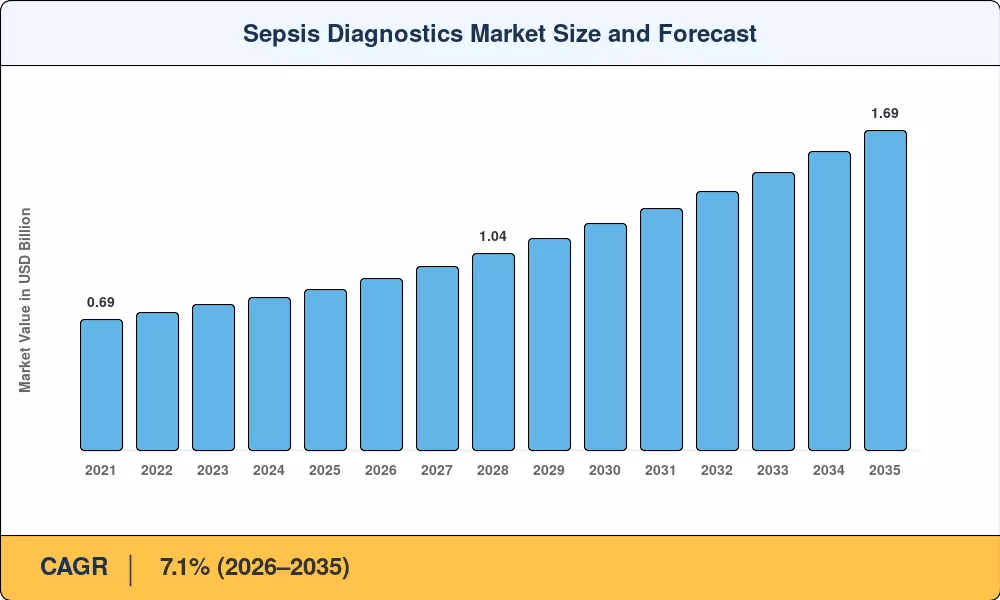

NY, CA, UNITED STATES, June 23, 2026 /EINPresswire.com/ — As per Market Research Future, the global Sepsis Diagnostics Market size to reach USD 1.69 Billion by 2035 from USD 0.91 Billion in 2026, at a CAGR of 7.1% during the forecast period 2026–2035. The market base was estimated at USD 0.85 Billion in 2025.

The 7.1% CAGR—anchored by structural infectious disease demand rather than discretionary healthcare spending—is driven by three converging forces: rising global sepsis incidence that continues to widen the addressable patient base for rapid pathogen identification, sustained molecular diagnostics technology shift that has displaced legacy blood culture systems with multiplex PCR and biomarker-driven platforms capable of returning actionable results in under three hours, and regulatory reimbursement mandates that have converted sepsis diagnostics from cost centers into reimbursement priorities tied to early intervention and antimicrobial stewardship compliance.

National governments and multilateral health organizations are amplifying this momentum. The WHO 2017 resolution declaring sepsis a global health priority spurred national surveillance mandates in over 40 countries. The Global Burden of Disease Study estimated 48.9 million sepsis cases and 11 million sepsis-related deaths in 2017, making sepsis responsible for nearly 20% of all global deaths.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/2110

Key Market Trends & Growth Drivers

Rising Global Sepsis Incidence and Extended Surveillance

The Global Burden of Disease Study estimated 48.9 million sepsis cases and 11 million sepsis-related deaths in 2017, making sepsis responsible for nearly 20% of all global deaths. Updated WHO surveillance data through 2023 indicates that sepsis incidence in low- and middle-income countries has increased by an estimated 12% since 2017, driven by expanding hospital access that paradoxically increases exposure to nosocomial pathogens.

This epidemiological trajectory creates a sustained volume floor for the Sepsis Diagnostics Market, ensuring that testing demand grows in parallel with healthcare system penetration, regardless of technology cycles.

National cancer registries in India and Brazil are also capturing higher detection rates as screening programs mature, feeding into the Sepsis Diagnostics Market growth pipeline across emerging economies. Each percentage point of sepsis incidence gain translates into measurable prescription volume for rapid pathogen identification, and the sepsis bundle compliance embedded in routine emergency and critical care makes this driver structurally durable through 2035.

Molecular Diagnostics Technology Shift

Legacy blood culture systems that require 24–72 hours for pathogen identification are being displaced by molecular and biomarker-driven platforms capable of returning actionable results in under three hours. The European Commission’s Horizon Europe program committed EUR 240 million between 2021 and 2027 to antimicrobial resistance diagnostics, a significant portion of which targets next-generation sepsis panels. Regulatory bodies, including the U.S. FDA, have fast-tracked clearances for multiplexed PCR-based sepsis panels, compressing approval timelines from 18 months to as few as 8 months under the Breakthrough Device Designation pathway.

Regulatory Reimbursement Mandates and Antimicrobial Stewardship

CMS’s SEP-1 core measure and its incorporation into the Hospital Value-Based Purchasing (VBP) Program tie provider reimbursement to early sepsis protocol compliance. This directly impacts a hospital’s capacity to completely recover the first 2% Medicare inpatient payment withhold since it links all-or-none bundle compliance to the composite Total Performance Score (TPS).

European data from the ECDC show that rapid pathogen identification reduces inappropriate antibiotic use by approximately 30–40% per patient. This economic and clinical incentive has driven hospital formulary committees to prioritize rapid molecular sepsis panels and biomarker testing protocols, shifting procurement budgets toward the Sepsis Diagnostics Market at the expense of reactive broad-spectrum antibiotic spending.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/2110

Market Segment Insights

BY TECHNOLOGY

Molecular Diagnostics: Dominant segment with ~36% revenue share in 2025. Reflecting entrenched hospital demand for rapid multiplex pathogen panels that reduce time-to-treatment. Multiplexed PCR panels such as the BIOFIRE FILMARRAY Blood Culture Identification Panel enable identification of over 40 pathogens and resistance markers directly from positive blood cultures in approximately one hour. Hospital procurement teams treat it as a default first-line platform, and expanding menu capabilities have enabled broad adoption even in cost-sensitive emerging markets.

Immunoassay: Fastest-growing technology segment at 7.8% CAGR (2026–2035). Driven by point-of-care procalcitonin and presepsin testing adoption in emergency departments. Emergency department adoption of rapid procalcitonin testing helps clinicians differentiate bacterial sepsis from viral infections and guide antibiotic de-escalation decisions.

BY PRODUCT

Assays and Reagents: Dominant product segment with ~52% revenue share in 2025. Driven by recurring consumable procurement cycles in high-throughput laboratories. Hospitals typically commit to multi-year reagent supply agreements tied to instrument placement contracts, generating predictable recurring revenue for manufacturers.

Instruments: Expanding segment as hospitals invest in automated platforms that integrate sample-to-answer workflows. Hospital capital equipment refresh cycles drive instrument replacement demand.

BY PATHOGEN

Bacterial Sepsis: Dominant pathogen type with ~68% revenue share in 2025. Consistent with epidemiological data showing that Gram-negative and Gram-positive bacteria cause over two-thirds of all confirmed sepsis episodes.

Fungal Sepsis: Fastest-growing pathogen segment at 8.3% CAGR (2026–2035). Reflecting the expanding population of immunocompromised patients—including organ transplant recipients, oncology patients, and individuals living with HIV—who are disproportionately susceptible to invasive Candida and Aspergillus infections.

BY APPLICATION

Clinical Diagnosis: Dominant application with the largest revenue share. Emergency department and ICU demand for rapid sepsis identification drives volume.

Drug Development: Growing application segment supporting pharmaceutical sepsis therapeutic trials.

Infection Control: Sustained demand from hospital infection prevention committees requiring rapid pathogen identification.

Research and Development: Academic and industry R&D applications for next-generation diagnostic platform validation.

BY END USER

Hospitals & Clinics: Largest end-user segment with the dominant share. Comprehensive emergency and critical care service lines dominate volume. Hospitals remain the primary delivery site for sepsis diagnostics due to laboratory infrastructure, specialized microbiology capacity, and regulatory compliance requirements.

Diagnostic Laboratories: Fastest-growing end-user segment. Reference laboratory networks and independent diagnostic facilities expanding sepsis testing menus.

Read Detailed Insights:

https://www.marketresearchfuture.com/reports/sepsis-diagnostics-market-2110

Regional Outlook

North America — Dominant Market (~38% Share, 2025)

The United States generates approximately 82% of North American Sepsis Diagnostics Market revenue, driven by the CMS SEP-1 mandate and payer compliance penalties, commercial insurance coverage of rapid molecular sepsis panels as first-line diagnostic protocols, and broad reimbursement for biomarker testing regimens—a single policy ecosystem that converted a delayed-diagnosis-dominated market into one with a structural early-intervention tail. CMS reimbursement for sepsis diagnostics under the Hospital Value-Based Purchasing Program has driven adoption in academic medical centers, while community hospitals increasingly prescribe point-of-care sepsis testing options to manage laboratory capacity. The US dominates through a combination of high per-patient spending, robust payer coverage, and rapid molecular diagnostics adoption.

Europe — Second Largest (~29% Share, 2025)

Europe’s Sepsis Diagnostics Market reflects divergent national strategies—Germany leads regionally with G-DRG incentives and a strong IVD manufacturing base, contributing ~24% of regional share, while the UK historically used selective diagnostic targeting before broadening coverage through NHS sepsis CQUIN targets at 7.3% CAGR. France contributes ~16% of regional share through national sepsis awareness campaigns and AMR policy. Italy contributes USD 0.03 Billion on regional hospital network upgrades. Spain is growing at 6.8% CAGR on public hospital diagnostic procurement expansion.

Asia-Pacific — Fastest-Growing Region (8.9% CAGR, 2026–2035)

Asia-Pacific is the engine of the Sepsis Diagnostics Market. China holds the largest regional share with ~34% of regional revenue, driven by the 14th Five-Year Plan county hospital investment—instantly extending sepsis diagnostic coverage to over 1.3 billion insured lives. India is growing at 9.6% CAGR on the back of Ayushman Bharat hospital modernization and the high sepsis mortality burden. Japan contributes ~22% of regional share through NHI pricing for advanced laboratory infrastructure at steady pace. South Korea is growing at 8.1% CAGR on National Health Insurance expansion for IVD.

Middle East & Africa — Emerging Opportunity (~6% Share, 2025)

The Middle East & Africa is bifurcated between well-funded Gulf states and resource-constrained Sub-Saharan nations. Saudi Arabia leads the region with Vision 2030 healthcare infrastructure investment, contributing ~28.6% of regional share—NEOM health cluster and the UAE’s premium hospital laboratory build-out have created pockets of excellence for sepsis diagnostics. The UAE is growing at 7.6% CAGR on medical tourism and premium hospital development. South Africa contributes ~18% of regional share on National Health Laboratory Service capacity.

South America — Growing Presence (~5% Share, 2025)

Brazil anchors South America’s Sepsis Diagnostics Market at ~58% of regional revenue, with the Unified Health System (SUS) driving centralized procurement tenders for blood culture systems and biomarker assays issued through state-level health secretariats, providing a stable demand floor that smooths regional forecasts. Access to advanced molecular diagnostics remains limited by import dependencies, though the Pan American Health Organization’s AMR surveillance initiative has catalyzed laboratory capacity investments across the region since 2021. Argentina is growing at 6.2% CAGR on private hospital laboratory expansion.

Competitive Landscape and Recent Developments

The Sepsis Diagnostics Market exhibits moderate concentration, with the top five players collectively holding an estimated 48–55% revenue share. The Herfindahl-Hirschman Index falls in the moderately concentrated range (approximately 1,200–1,500), reflecting a mix of large diversified IVD corporations and specialized sepsis-focused innovators. Strategic activity centers on platform expansion through acquisitions, reagent menu broadening, and AI integration partnerships.

The competitive landscape is stratified between molecular diagnostics pioneers serving global sepsis testing markets, integrated platform expansion specialists capturing laboratory automation tenders, and point-of-care developers consolidating the emergency department segment.

KEY COMPANIES AND RECENT MILESTONES

bioMérieux (2024–2025): Maintains leadership with the BIOFIRE FILMARRAY Blood Culture Identification Panel and VIDAS B·R·A·H·M·S PCT, commanding ~12–15% of global Sepsis Diagnostics Market revenue. Integrated molecular-immunoassay portfolio leader with global sepsis testing leadership. Premium platform positioning in specialty segments offsets price compression in competitive markets.

Becton Dickinson (BD) (2024–2025): BD BACTEC Blood Culture Systems and BD MAX System reinforce blood culture installed base dominance, holding ~10–13% of global revenue. The company benefits from the structural molecular diagnostics tail created by expanded platform menu investment.

Roche Diagnostics (2024–2025): Elecsys BRAHMS PCT and cobas Liat System reinforce centralized and POC immunoassay breadth positioning, holding ~8–11% of global revenue. Announced collaboration with Sepsis Alliance to fund clinical validation studies for next-generation procalcitonin algorithms integrated into the cobas platform.

Danaher (Beckman Coulter / Cepheid) (2024–2025): GeneXpert Sepsis Panels and DxH Hematology Analyzers reinforce rapid molecular POC and lab automation positioning, holding ~7–10% of global revenue. Expanded GeneXpert sepsis panel menu to include additional antimicrobial resistance gene targets, addressing stewardship program requirements.

Thermo Fisher Scientific (2024–2025): MicroScan WalkAway Systems and Applied Biosystems Platforms reinforce microbiology and molecular dual presence positioning, holding ~6–9% of global revenue.

Abbott Laboratories (2024–2025): ARCHITECT BRAHMS PCT and Alinity Systems reinforce broad immunoassay and integrated diagnostics positioning, holding ~5–8% of global revenue.

Future Outlook: 2026–2035

By 2030, precision molecular diagnostics and AI-integrated clinical decision support will become the operating system of sepsis management. The convergence of rapid pathogen identification and predictive analytics will reshape the Sepsis Diagnostics Market through the late 2020s. By 2030, an estimated 40% of newly diagnosed sepsis cases in academic medical centers will undergo multiplex PCR pathogen identification followed by matched antimicrobial therapy, creating a diagnostic-therapeutic revenue loop.

The European Commission’s EUR 240 million Horizon Europe investment ensures next-generation panel supply scales alongside clinical demand. Machine-learning models that integrate vital signs, laboratory values, and electronic health record data can predict sepsis onset 4–6 hours before clinical recognition. Start-ups have raised significant venture funding for sepsis decision-support tools since 2023.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/infectious-disease-diagnosis-treatment-market-7031

https://www.marketresearchfuture.com/reports/molecular-diagnostics-market-1171

https://www.marketresearchfuture.com/reports/blood-screening-market-6899

https://www.marketresearchfuture.com/reports/microbiology-testing-market-697

https://www.marketresearchfuture.com/reports/in-vitro-diagnostics-market-1165

https://www.marketresearchfuture.com/reports/point-of-care-diagnostics-testing-market-10642

https://www.marketresearchfuture.com/reports/clinical-laboratory-services-market-7145

https://www.marketresearchfuture.com/reports/biomarker-market-1941

https://www.marketresearchfuture.com/reports/immunoassay-market-5841

https://www.marketresearchfuture.com/reports/hospital-acquired-infections-market-2576

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery